Market Commentary: 8 April 2026

Please note that the content of this review should not be considered as investment advice or any form of recommendation. If you require investment advice, please do not hesitate to get in touch with a member of our qualified team.

Stocks Rise on Middle East Ceasefire

• Stock markets (MSCI World Index) have only declined by 4.1% since the Iran conflict began.

• Bond markets (Bloomberg Global Aggregate Index) have declined by 2.8%.

Key Themes

The number of ships passing through the Strait of Hormuz has been severely restricted in recent weeks, at roughly 5% of usual levels.1 This has created a supply crisis in the oil, natural gas and fertiliser markets.2 However, a two-week ceasefire has just been agreed, leading to a strong bounce in financial markets this morning. Overall, stocks have acted stoically in the face of the crisis, experiencing relatively modest declines to date.

UK

It is sometimes said that financial markets react to two primary drivers: growth and inflation. Stocks perform best when economic growth is high and inflation is low.3 However, an energy supply crisis creates the opposite effect by reducing growth and increasing inflation. The OECD suggests Britain could be the hardest hit of the G20 economies, with inflation potentially rising to 4%.4 The Chancellor will certainly hope that today’s ceasefire announcement does mark the beginning of the end, with the markets and economy allowed to return to normal without lasting damage being sustained.

The FTSE 100 has remained relatively resilient, helped by its international oil & gas companies such as BP and Shell. Small cap stocks have been hit much harder, with the AIM All-Share Index declining by 15% in one month.

United States

US stocks experienced their worst start to a year since 2022, albeit the first quarter did end with the best single-day rise since last May.5 Back then, there was a sharp recovery as Trump backed down from the worst of his tariff threats. Investors are now hoping for a similar bounce.

US employment data was better than expected last week, and analysts’ earnings forecasts have actually increased since the conflict began. Only one-fifth of S&P 500 companies have had their forecasts reduced, despite the spike in energy prices.6 Some might argue this is a sign of complacency, others might say they are looking through the current headlines to the potential for strong growth later in the year.

Europe

In Europe, defence contractors extended their recent outperformance, banks remained resilient and pockets of the renewables sector showed signs of stabilisation. Danish firm Orsted is the world’s largest offshore wind provider, accounting for one-quarter of global capacity, and its shares have gained 40% in six months. However, the share price remains almost 90% lower than its peak 2021 level after a long period of decline caused by higher construction costs, higher interest rates and Trump’s attempts to ban its flagship US developments.

Asia & Emerging Markets

South Korea’s stock market has experienced a rollercoaster ride this year. Samsung and its competitor SK Hynix make up more than 40% of the KOSPI index and supply two-thirds of global computer memory.7 The KOSPI gained 60% in January and February due to surging demand for DRAM within AI data centres, but fell 20% when the Strait of Hormuz closure blocked the supply of energy and helium, which is a key manufacturing component. With the index up 7% this morning, South Korea would be one of the clearest beneficiaries from a lasting ceasefire.

Bonds

The bond market has neatly encapsulated the growth and inflation narratives related to the conflict. 10-year gilt yields rose sharply from 4.3% to 5.0% due to the initial inflation scare from rising oil prices. Later in March yields started to decline, factoring in the potential knock-on effect of lower economic growth. Yields moved lower once again this morning on the ceasefire announcement and now stand at 4.7%. This remains an elevated level, which may prevent the return of the cheap mortgage deals that had started to appear earlier in the year.

Points of Interest

Before the conflict began, the price of oil was very close to its post-WW2 average when adjusted for inflation.8 However, it was historically cheap by another measure. One ounce of gold could buy 78 barrels of West Texas Intermediate crude in February – a level only matched during the Covid lockdowns in 2020, and far surpassing the 10 to 30 barrel range which existed during the previous 80 years.9

Summary

There is a method of investing which says “if the problem is large enough, buy the problem”. This has worked very well in recent years. When a pandemic caused the global economy to freeze, governments injected a massive amount of money into the financial system and stock markets boomed higher for 18 months. When Trump threatened to derail global trade last spring through a complex and punitive tariff system, he backed down and stocks quickly rose to new highs. Will today’s ceasefire create another lasting rally, or will the “buy the dip” trend finally end? The initial market reaction is signalling the former, but developments over the following days and weeks will prove crucial.

Note: Past Performance Is Not A Reliable Indicator Of Future Performance

Sources may be found online here, or provided on request

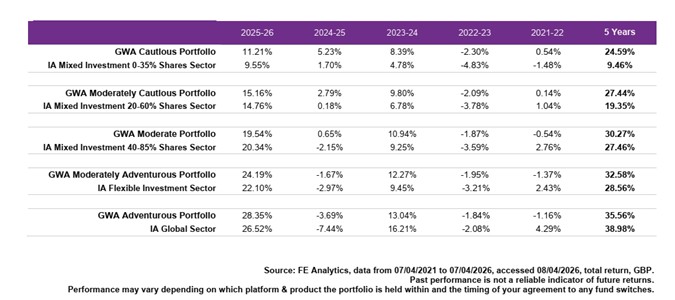

GWA Portfolio Performance

Please note that any performance figures are provided for information purposes only. The performance of your own investments may deviate from the returns shown below due to a number of factors, including product charges, the timing of contributions & withdrawals and portfolio rebalancing. Performance relates to the GWA Portfolios only; if you hold other investments performance will be different.

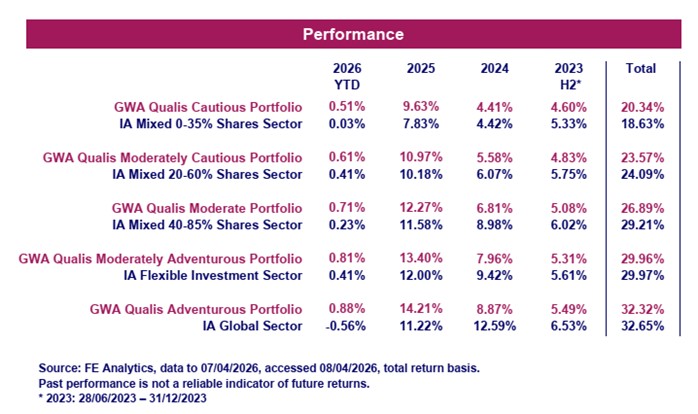

The MGTS Qualis Funds

Please note that this should not be considered as investment advice or any form of recommendation or inducement to invest. If you require investment advice, please contact your financial adviser.

The MGTS Qualis Funds launched in June 2023 and are managed by our wholly owned subsidiary, GWA Asset Management Ltd.

Fund Positioning

The MGTS Qualis Defensive Fund invests mainly in fixed income funds, which hold government bonds and corporate bonds. The fund also invests in other assets, such as property and infrastructure.

The MGTS Qualis Growth Fund invests solely in equities and is focused upon geographic diversification. The fund has a broad range of investments across the UK, US, Europe and Asia.

For further information including the latest Fund Factsheets, please visit qualisfunds.co.uk