Scotland vs England – A Taxpayer Comparison *UPDATED*

We have recently updated our Scotland vs England Taxpayer comparison from our original blog post of January 2024.

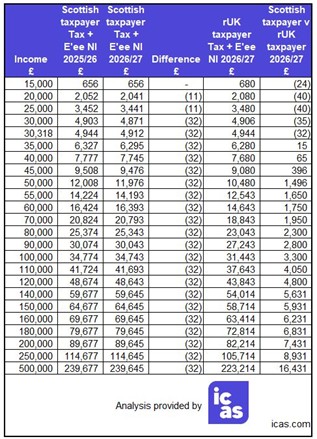

Following the Scottish Budget on 13 January 2026, The Institute of Chartered Accountants Scotland (ICAS) has updated their table comparing the amount of Income Tax and National Insurance Contributions (NICs) that an employee resident in Scotland would pay compared to the rest of the UK. Whilst the Welsh Parliament has the ability to vary Income Tax rates in Wales, these are, for now, aligned with Income Tax rates in England and Northern Ireland.

The Scottish rate of Income Tax only applies to certain sources of income (e.g. employment, self-employment, rental income). It does not apply to savings and dividend income which continue to be taxed per the rates and bands set by Westminster.

The recent Scottish Budget has made substantial (7.4%) increases in the Scottish Starter rate and the Scottish Basic rate. However, the Scottish Higher rate of Income Tax continues to start from £43,663 of income. This means that the marginal rate of tax and NICs for someone earning between £43,663 and £50,270 is 50% (being 42% income tax and 8% Class 1 Employee NICs).

Even at modest income levels (£50,000), there is at a differential of almost £1,500 in take home pay between a Scottish and English resident taxpayer.

At higher income levels, the differential is even starker. Take an employee relocating to Scotland. In England they earn £100,000 (with take home pay of £68,557). In Scotland, the employee’s take home pay would be £65,257 on the same income of £100,000. To provide the employee with the same amount of take home pay, they would have to earn £110,820. The reason for this is that the marginal rate of tax for a Scottish resident employee is 69.5% for earnings between £100,000 and £125,140 (i.e. 45% Income Tax, 2% Employee NICs and an additional 22.5% due to the loss of the Income Tax personal allowance where taxable income exceeds £100,000).

One way or another, that £10,820 differential in gross pay is purely Tax and NICs.

Source: icas.com