Market Commentary: 10 March 2026

Please note that the content of this review should not be considered as investment advice or any form of recommendation. If you require investment advice, please do not hesitate to get in touch with a member of our qualified team.

Markets Upended By Middle East Conflict

- Most stock markets have declined between 5% and 10% since the US & Israel attacked Iran on 28 February.

- Bonds have also declined, due to the uptick in inflation that is likely to follow

Key Themes

The stock market has suddenly pivoted from fixating on the very new technology of artificial intelligence to the very old problem of conflict in the Middle East. With war as the dominant theme, many of the market’s prior assumptions have been turned on their head. Stocks quickly gave back their 2026 gains, as Brent crude breached $100 per barrel for the first time since Russia’s invasion of Ukraine in 2022. The inflationary impact could be significant, if the conflict drags on. However, investors will hope that President Trump claims a quick win, allowing markets to return to their previous state.

UK

On some days last week, it appeared as though the only shares making gains in the FTSE All Share were energy and defence companies, with the rest of the market declining significantly. Housebuilding and travel stocks were among the worst affected. However, the index remains up slightly year-to-date and has been more resilient than Asian and European markets since the conflict began.

Initial estimates suggest a spike in oil prices could add up to 0.8% to UK inflation over the next year (with CPI last recorded at 3.0%).1 There could also be a negative impact on economic growth.

United States

In the months prior to the attack, US stocks were producing lower returns than other developed markets and the US dollar was declining against major currencies. Those trends quickly flipped, with US stocks proving the most defensive since 28 February and the dollar rising in value due to its “safe haven” status.

Following its shale fracking revolution, the US is now the largest oil producer in the world accounting for 20% of global output.2 However, it isn’t immune to the negative effects of higher oil prices. The cost of living was already the top concern among voters, and US motorists are highly sensitive to the cost of “gas” at the pump.3,4 Therefore, Trump will face pressure to bring energy prices down ahead of key midterm elections in November. Those elections will determine which party controls Congress for the final years of his presidency, and they could also affect his legacy as a vote-winner.

Europe

Compared to the UK, continental Europe has greater exposure to car manufacturers (such as Volkswagen and Mercedes-Benz) and industrial exporters (such as Airbus), with fewer energy and commodity companies. This explains why the region’s stocks have been harder hit than the UK’s. The German, French, Italian and Spanish stock markets have all declined by more than 8% since the conflict began.

Asia & Emerging Markets

When a “risk off” mood emerges, investors often react by selling the holdings that have risen the most, to book gains and raise cash. Japanese and Emerging Market stocks rose 15% in the first 8 weeks of 2026 – more than double the return of many other regions. It is no surprise they have suffered some of the sharpest declines since the conflict began. In Japan’s case there is also a fundamental reason: almost all of its energy it imported, and almost all its oil is sourced from the Middle East – making it particularly vulnerable to the current crisis.5

Bonds

Government bond yields have risen due to the conflict, as inflation expectations have increased. This could have an unwelcome effect on the UK mortgage market. With 2-year and 5-year gilt yields rising 0.45 percentage points, there is pressure for fixed term mortgage rates to increase by a similar amount. It is unfortunate timing, as they had been on a declining trend beforehand.6

In the US, concerns about private credit markets have grown in recent months. This is where large asset managers lend money to companies privately, away from the public markets. An estimated $1.7 trillion of such loans are thought to exist, with many being made to private equity companies and the software sector. Opaque and illiquid, private credit funds are now facing significant outflows amid warnings that default rates could prove much higher than expected.7

Points of Interest

In happier news, many people have been vexed by the spiralling cost of chocolate but a reprieve could finally be on the horizon. Global cocoa prices surged from £1,750 to £9,000 per tonne between 2022 and 2025, following a series of crop failures in West Africa. However, supply is now recovering and prices dipped back to £2,000 per tonne at one point last week.8 All eyes will now turn to supermarket shelves for signs of price reductions in the coming months.

Summary

The Iranian conflict threatens to reverse many of the clear themes that have underpinned financial markets in recent months. Interest rates were expected to fall this year in response to lower inflation. That may not transpire, unless the situation is resolved quickly. A sustained energy price shock would also undermine forecasts for strong economic growth by increasing costs for households and businesses. However, we should bear in mind that Trump’s presidency has produced several scares and each of them has been transitory, up to now. Amid turbulence, it is best to sit tight and wait for the skies to clear.

Note: Past Performance Is Not A Reliable Indicator Of Future Performance

Sources may be found online here, or provided on request

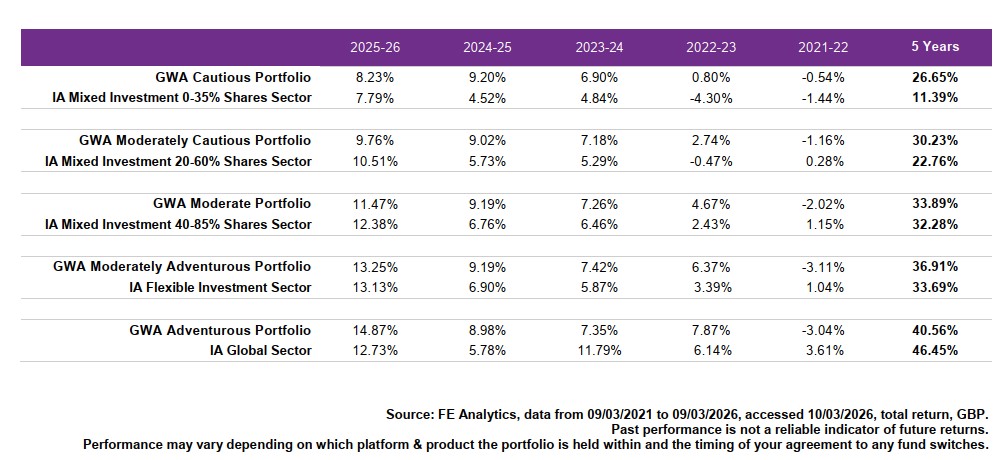

GWA Portfolio Performance

Please note that any performance figures are provided for information purposes only. The performance of your own investments may deviate from the returns shown below due to a number of factors, including product charges, the timing of contributions & withdrawals and portfolio rebalancing. Performance relates to the GWA Portfolios only; if you hold other investments performance will be different.

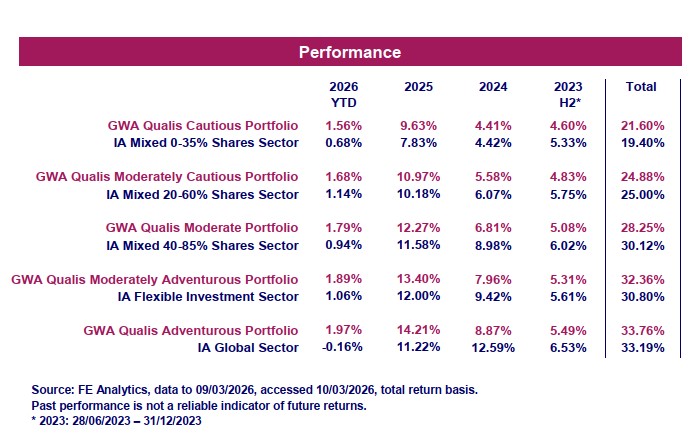

MGTS Qualis Funds

Please note that this should not be considered as investment advice or any form of recommendation or inducement to invest. If you require investment advice, please contact your financial adviser.

The MGTS Qualis Funds launched in June 2023 and are managed by our wholly owned subsidiary, GWA Asset Management Ltd.

Please note that this should not be considered as investment advice or any form of recommendation or inducement to invest. If you require investment advice, please contact your financial adviser.

Fund Positioning

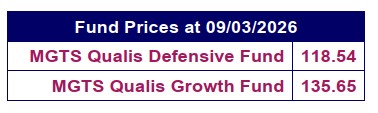

The MGTS Qualis Defensive Fund invests mainly in fixed income funds, which hold government bonds and corporate bonds. The fund also invests in other assets, such as property and infrastructure.

The MGTS Qualis Growth Fund invests solely in equities and is focused upon geographic diversification. The fund has a broad range of investments across the UK, US, Europe and Asia.

For further information including the latest Fund Factsheets, please visit qualisfunds.co.uk